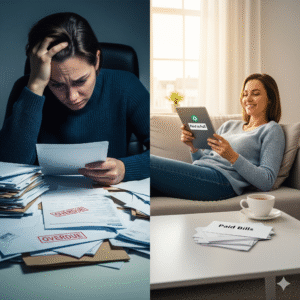

Reviews of Freedom Debt Relief reminded me of a buddy who was under stress due to credit card debt. Collectors kept calling, and he was confused of where to start. After he got in touch with Freedom Debt Relief, they helped him figure out a simple plan, handle his creditors, and roll all his payments into one easy monthly bill, manageable monthly sum. He felt in control at last, and the procedure was simple to understand. It was more important to him to have peace of mind and not be under constant worry than it was to pay off his debt.

If you’re struggling with debt and seeking a solution, you may have come across Freedom Debt Relief. Let’s start the review.

Freedom Debt Relief Reviews: Is it worth it?

Reading about Freedom Debt Relief reminded me of a friend of mine who was drowning in credit card debt. He used to get calls from collectors all the time and his mind was spinning as to where to start. Then he contacted Freedom Debt Relief, and they gave him an easy plan.

They talked to the creditors on his behalf and changed all the different payments into a manageable monthly amount. The biggest thing he got was control and peace of mind… now he is not in constant tension.

If you are also in a similar situation, then you must be thinking whether this company is good or not. Come, let’s understand it like a friend.

What is Freedom Debt Relief?

Simply put, it is a debt settlement company. Their job is to talk to your creditors (whose money you have borrowed) and settle them in less money.

How Does It Work?

- Instead of giving money directly to the creditors every month, you put money in a separate account.

- When enough money accumulates in it, then the people of Freedom Debt Relief talk to your creditors.

- They settle in a lump sum amount which is less than your actual debt.

Feeling good, isn’t it? But in money matters there is always another aspect too. Let’s see the good and bad points.

Good Points (Pros)

- No fee upfront: You don’t have to pay anything until they settle your debt successfully.

- Single Payment: Making all separate payments in one reduces mental stress to a great extent.

- They handle the stress: They take the stress of collector calls and gossip, not you.

- Experience: They have been there for a long time and have settled the debt of lakhs of people.

Bad Points (Cons)

- Credit Score Will Fall: This is the biggest point. If you stop paying money directly to creditors, your credit score will fall.

- Settlement is not guaranteed: Not every creditor is accepted. It is possible that someone may not be able to settle.

- Fees are charged: They take 15% to 25% of your accumulated debt. These fees affect your savings.

- It does not happen quickly: This process can take 2 to 4 years. It is not a quick work.

What Are People Saying? (Real Customer Reviews)

- People’s reviews are mixed, which shows that this is not for everyone.

- “Freedom Debt Relief helped me settle my $20,000 credit card debt. Yes, my credit score had fallen before, but now I am finally debt-free!” – Mark S.

- “They settled some debts, but not all. I wish I would have looked at other options before signing up.” – Lisa R.

- “Customer service was good, but I had no idea my credit score would drop this much.” – Dave M.

So, Is Freedom Debt Relief Legit?

Absolutely. It’s a legitimate company. But being “legit” doesn’t mean it’s right for you.

One important thing: In 2019 they had to settle with a government agency over some misleading practices. They have made changes, but you should make that decision after knowing it.

What Other Options Do You Have?

This is the most important part of your research. Debt settlement is one way out, but not the only one.

1. Debt Management Plan (DMP)

Work with a non-profit credit counseling agency. They can help lower your interest rates and combine payments without hurting your credit score too much.

2. Debt Consolidation Loan

If your credit score is still good, you can pay off all your debts with one loan. Then you only have to repay one loan, which has a lower interest rate.

3. Creating Your Own Budget

Some people create a strict budget (like the debt avalanche or snowball method) without anyone’s help. You can still get out of debt.

Finally: Should You Use It?

Freedom Debt Relief may work for you if:

- Your unsecured debt is very high (e.g. $15,000 or more).

- You are falling behind on payments and are unable to make minimum payments.

- You think your credit score is going to drop.

- You have tried options like a Debt Management Plan or not.

It is not the best choice for you if:

- Your debt is small or you still make payments on time.

- Your credit score is very important for you in the coming time (like planning to buy a house).

- You are looking for a quick and easy way.

In the end, my brother/sister, the best choice is the one in which you take a decision with complete information. Do your homework, look at these alternatives, and choose the path that gives you both a clear financial future and peace of mind.

Read More: Yrefy Reviews: Is It the Right Choice for You? ❤️

FAQs (Frequently Asked Questions)

Most of these debts are unsecured, such as personal loans and credit cards. Secured debts such as vehicle loans, mortgages (house loans), and school loans are often not handled by it.

Although the majority of people believe that the minimum should be $7,500, it is often more effective to have $15,000 or more.

During the program, you may skip paying your expenses, which might cause your score to plummet dramatically. Once the program is over and the debts are paid off, you can raise your credit score once more.

24 to 48 months, on average.

The amount of money they save you will determine this. Even if they impose a 20% fee ($1,000) and settle your $10,000 debt for $5,000, you will still save $4,000. Always do your math.

Yes, the firm has been in operation for more than 20 years and is licensed.

No. Only once a settlement has been reached and accepted by you do you make payment.

Although savings vary, typically consumers pay 40–60% of the total amount due before fees.

Only unsecured debts, please. Typically, things like school debts and mortgages are not eligible.

The relief of being debt-free, helpful personnel, and no upfront costs.